Ontario Auto Insurance Reform 2026 Explained for Drivers

If you have a car registered in Ontario, you need to be aware of the Ontario auto insurance reform 2026 updates that apply starting July 1, 2026. The province is overhauling how accident benefits work under your auto insurance policy, and some of the changes are significant. This guide breaks down exactly what is changing, how it could affect my insurance premiums and coverage, and what steps you should take before the deadline.

What Is the Ontario Auto Insurance Reform 2026?

Ontario is implementing an auto insurance overhaul on July 1, 2026. The core change is this: many accident benefits that were previously automatic and included in every auto insurance policy will become optional. You will need to choose and pay for them if you want them actively.

The overhaul shifts Ontario from a bundled insurance model to an “à la carte” system of accident benefits optionality, where drivers can customize their auto insurance coverage based on their personal situation. The government frames this as giving drivers more choice and potentially lower insurance premiums. That flexibility is real, but so are the risks if you opt out without fully understanding what you are giving up.

What Are Statutory Accident Benefits (SABS)?

Statutory accident benefits, often referred to as SABS, are a form of no-fault coverage that comes with every Ontario auto insurance policy. They provide financial support if you are injured in a car accident, regardless of who caused the collision.

Currently, these benefits cover a wide range of needs after an accident, including:

- Medical and rehabilitation expenses

- Lost income if you cannot work

- Caregiver costs if you care for a child or aging parent and can no longer fulfill that role.

- Death and funeral benefits for your family

- Housekeeping and home maintenance, if your injuries prevent you from managing those tasks

The statutory accident benefits schedule (SABS) sets out what each of these covers and at what level. The 2026 reform fundamentally restructures this schedule.

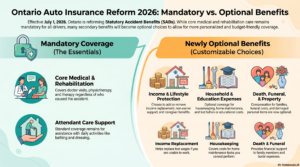

What Stays Mandatory After July 1, 2026

Standard medical or rehabilitation benefits will remain mandatory in all auto insurance policies, as will attendant care benefits. These three form the foundation of what the province considers essential recovery support after a collision.

To be clear, these mandatory benefits include:

- Medical and rehabilitation benefits: These cover reasonable and necessary expenses like medical treatment, physiotherapy, prescription medication costs, and supplementary medical rehabilitation support.

- Attendant care benefits: These cover the cost of a professional caregiver if your injuries require personal assistance during recovery.

You can also purchase optional benefits beyond the mandatory levels, such as supplementary medical, rehabilitation, and attendant care coverage, which were already available as certain accident benefits coverage before this reform. The base protection stays in place for everyone. What changes is everything built on top of it.

What Becomes Optional Starting July 1, 2026

This is where the reform has the biggest practical impact. Nine newly optional benefits that were once automatically included in every personal private passenger auto policy will now require a separate choice. They are not being eliminated, but you will need to specifically add them and pay for them.

The benefits that will become optional include:

- Income replacement benefits: This covers a portion of your lost income if a car accident prevents you from working. Under the current system, it pays up to $400 per week. Income replacement benefits will become optional starting July 1, 2026.

- Non-earner benefits: Designed for students, retirees, or unemployed individuals who are completely unable to carry on a normal life after an accident.

- Caregiver benefits: Cover caregiving expenses if you are injured and can no longer care for a dependent, such as a child or an aging parent. Caregiver benefits will also be optional as of July 1, 2026.

- Housekeeping and home maintenance benefits: Helps if your injuries prevent you from maintaining your home.

- Lost educational expenses: Compensates for educational expenses you lose because of an accident-related interruption to an education program.

- Expenses of visitors: Covers reasonable expenses of visitors who come to see you during your hospital stay or recovery.

- Damage to personal items: Helps replace clothing, prescription eyewear, hearing aids, and other personal items damaged in the accident.

- Death benefits: Provide financial compensation to family members, including the named insured’s spouse, persons who are dependants, or another covered person, if a covered person dies as a result of an accident.

- Funeral benefits: Cover some of the funeral expenses if a covered person dies due to an auto accident.

All other statutory accident benefits will become optional in Ontario’s new insurance model. For context, indexation and dependent care benefits were already optional benefits before this reform and will continue to be offered by health insurance providers as add-ons to your auto policy.

Checkout:

- Ontario Auto Insurance Renewal Checklist 2026

- How OPCF 47R Changes Ontario Auto Insurance in 2026

- Ontario Auto Insurance Reform 2026 Explained for Drivers

Who Is Actually Covered for Optional Benefits

This is one of the most important and least understood aspects of the 2026 reform. As of July 1, 2026, only the coverage under optional benefits will apply to named insureds and their dependents, which is one of the most consequential shifts in how both your auto insurance and private plans interact. More specifically, optional accident benefits coverage will extend only to:

- The named insured on the policy

- The named insured’s spouse.

- Dependents of the named insured and of the named insured’s spouse

- Drivers listed on the policy

This represents a significant narrowing compared to the current system. Passengers, pedestrians, and cyclists who fall outside these categories may no longer be eligible for optional benefits under someone else’s policy. Pedestrians and cyclists may lose coverage for optional benefits after July 1, 2026, unless they have their own auto insurance policy that includes optional coverage.

The mandatory benefits, meaning medical, rehabilitation, and attendant care, will still apply to passengers, pedestrians, and cyclists involved in a collision. But anything beyond that core coverage will not be available to them through the at-fault driver’s optional coverages, regardless of what optional coverages were purchased on that policy.

The “First Payer” Rule: A New Order for Medical Claims

Ontario’s 2026 reform also introduces a change to how medical and rehabilitation costs are paid. Starting July 1, 2026, your auto insurance will pay first for accident-related medical and rehabilitation expenses, ahead of your workplace benefits or private health plan.

Previously, many people relied on their employer’s supplementary health insurance plan as a primary source of recovery support. Under the new model, your auto insurance provider becomes the first payer for medical and rehabilitation costs, excluding medication, before your Ontario health insurance plan, private benefits plan, or personal or work benefits take over.

This has a direct implication: drivers should review existing workplace health benefits to avoid coverage duplication. If your employer’s plan already provides strong coverage, you may not need to purchase every optional benefit available. On the other hand, if your private health plan is limited, you may want to keep more optional benefits in place.

How the Reform Affects Different Types of Drivers

The new model does not affect everyone the same way. Your situation matters.

Self-Employed Workers and Contractors

If you are self-employed, you likely do not have access to an employer-sponsored disability plan. Income replacement benefits will be one of the most important optional benefits for you to keep. Without it, a serious car accident could leave you without any income during your recovery.

Parents and Caregivers

If you care for children or an aging parent, caregiver benefits cover the cost of a replacement caregiver when you cannot fulfill that role due to accident-related injuries. Without this benefit in place, those caregiving expenses come directly out of your pocket during what is already a difficult time.

Students

Students who are involved in a car accident and cannot continue their education program may qualify for non-earner benefits and lost educational expenses coverage. Both of these become optional under the 2026 reform. Self-employed individuals, students, and caregivers may face financial risks if opting out of coverage, so it is worth reviewing your specific situation carefully.

Drivers with Strong Workplace Benefits

If you have a comprehensive private benefits plan through your employer, you may have some overlap with optional benefits. In that case, removing optional benefits can reduce what you pay, but you should first understand how removing optional benefits could affect your insurance and leave gaps that a robust auto insurance coverage plan could otherwise fill. Just make sure the overlap is real and not assumed. Some workplace plans have limits or exclusions that leave gaps that a robust auto insurance policy could cover.

What Happens to Your Existing Policy

If you already have an Ontario auto insurance policy, your coverage will not automatically change. Your policy renews automatically unless you request changes. This means existing customers retain their current coverage unless they actively choose to make modifications.

However, the eligibility rules for optional benefits change on July 1, 2026, regardless of your renewal date. Even if your auto policy does not renew until later in the year, who is covered by your optional benefits is narrowed to that date.

If you want to remove optional benefits and potentially reduce your premium, you must agree to the changes in writing with your insurer. If you are purchasing a new policy on or after July 1, 2026, only the mandatory benefits will be included by default. You choose which optional benefits to add from there.

How to Prepare Before July 1, 2026

Review your current coverage before making changes. That is the most important thing you can do right now. Here is a practical approach:

- Check your workplace or private benefits plan. Understand what your employer or supplementary health insurance plan covers before removing any auto insurance benefits. Check for coverage duplication with workplace benefits to avoid paying for the same protection twice.

- Think about your personal situation. Are you self-employed? Do you have dependants? Do you have an aging parent you care for? These factors directly affect which optional benefits make sense for you.

- Talk to a licensed broker. The new model is more customizable, but that also means more complex. A broker can walk you through your options and help you understand how the changes affect your specific policy.

- Do not wait for your renewal. The eligibility changes take effect July 1, 2026, across all policies. Do not assume your renewal date is the trigger for action.

Ready to Review Your Coverage?

At Acumen Insurance, we help Ontario drivers understand their options and make confident decisions about their auto insurance policy. Whether you want to review your current coverage, add optional accident benefits, or build a policy that fits your life, our team is here to help.

Contact Acumen Insurance today to speak with a licensed broker before July 1, 2026. The right coverage starts with the right conversation.

Ontario Auto Insurance Reform 2026 – FAQs

What is changing about Ontario auto insurance on July 1, 2026?

The reform makes most auto insurance accident benefits optional rather than automatic. Only medical, rehabilitation, and attendant care benefits remain mandatory. Everything else, including income replacement and caregiver benefits, must be actively chosen and added to your policy.

Will my existing coverage change automatically on July 1, 2026?

No. Existing policies renew with the same coverage and limits unless you agree in writing to change them. However, who qualifies for your optional benefits will be narrowed on July 1, 2026, regardless of your renewal date.

Can I add optional benefits back after July 1, 2026?

Yes. You can change optional benefits at any time. Speak with your broker to understand the process and any conditions that may apply.

Who does optional accident benefits coverage apply after the reform?

Optional benefits will only apply to the named insured, their spouse, their dependants, and listed drivers on the policy, and you cannot remove optional accident benefits from certain covered persons without them applying to all of them. Passengers, pedestrians, and cyclists outside those groups are not covered for optional benefits under your policy.

What happens to pedestrians and cyclists after July 1, 2026?

Mandatory benefits, meaning medical, rehabilitation, and attendant care, still apply to uninsured pedestrians and cyclists hit by a vehicle. However, they will not have access to optional benefits through the at-fault driver’s policy unless they are a listed dependent or driver on that policy.

Will opting out of optional benefits lower my insurance premiums?

It can. Removing coverage reduces your premium, but it also removes the financial protection that coverage provides. Review your private and workplace benefits first, and consult a broker before making any decisions.

What is the “first payer” rule introduced in the 2026 reform?

Under the new rules, your auto insurer pays first for accident-related medical and rehabilitation costs before your workplace or private health plan. This changes the order in which claims are processed and is worth factoring into how you coordinate your benefits.

I am self-employed. Which optional benefits matter most for me?

Income replacement benefits are especially important if you are self-employed and do not have a group disability plan through an employer. Losing that coverage after an accident could leave you without income during your recovery.

What if I am buying a new policy after July 1, 2026?

New customers purchasing a policy on or after July 1, 2026, will only receive the mandatory minimums by default. You will need to choose which optional accident benefits to add at the time of purchase.

Where can I get help understanding how the reform affects my specific policy?

A licensed Ontario insurance broker is the best resource. They can review your current auto insurance policy, explain what changes affect you, and help you decide which optional benefits are worth keeping.

Blog